You’ll need a few items to perform a bank reconciliation, including your bank statement, internal accounting records, and a record of any pending cash transactions (either inflows or outflows). A bank reconciliation statement can help you identify differences between your company’s bank and book balances. The bank reconciliation is prepared as a statement called the Bank Reconciliation Statement (not to be confused with the bank statement which you received from the bank). The reconciliation should be prepared on a regular basis (daily, weekly or monthly) dependent on the size of the firm and how many transactions are being processed through the cash book. Miscellaneous debit and credit entries in the bank statements must be recorded on the balance sheet.

Reduced human errors

Note that the transactions the company is aware of have already been recorded (journalized) in its records. However, the transactions that the bank is aware of but the company is not must be journalized in the entity’s records. Most differences highlighted by the bank reconciliation procedure are due to timing differences as one organisation may have posted an item which the other has not.

First, check your two cash balances

Mitch has more than a decade of experience as personal finance editor, writer and content strategist. Before joining Forbes Advisor, Mitch worked for several sites, including Bankrate, Investopedia, Interest, PrimeRates and FlexJobs. Kevin has been writing and creating personal finance and travel content for over six years.

How do you prepare a bank reconciliation statement?

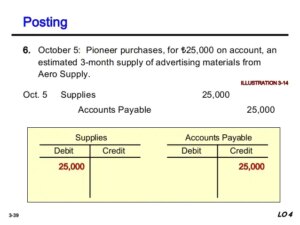

This first document, or rather a ledger, is the bank book of the company. The bank is an internally prepared document that shows the company’s side of transactions. The company carries over the balance from its bank book to its trail balance and, subsequently, its financial statements. Therefore, the bank book is an important document in the accounting process of a company. This can also help you catch any bank service fees or interest income making sure your company’s cash balance is accurate.

We’ll go over each step of the bank reconciliation process in more detail, but first—are your books up to date? If you’ve fallen behind on your bookkeeping, use our catch up bookkeeping guide to get back on track (or hire us to do your catch up bookkeeping for you). Any credit cards, PayPal accounts, or other accounts with business transactions should be reconciled. After adjusting the balance as per the cash book, make sure that you record all adjustments in your company’s general ledger accounts.

- That part of the accounting system which contains the balance sheet and income statement accounts used for recording transactions.

- There’s nothing harmful about outstanding checks/withdrawals or outstanding deposits/receipts, so long as you keep track of them.

- During September, the company received $120,000 from sales and invoiced debtors $40,000 the previous month, and received a check that has not yet been reflected in the bank account.

- If there are still some differences, these may be due to errors in either the two balances or the bank reconciliation process.

- Then, you make a record of those discrepancies, so you or your accountant can be certain there’s no money that has gone “missing” from your business.

In doing so, it reduces the time and effort required for manual reconciliation. Preparing a bank reconciliation involves matching your company’s financial records with your bank statements to ensure consistency and identify bookkeeping questions any discrepancies. Bank reconciliation is a crucial financial process for businesses to ensure that records match bank statements. In this post, we’ll explore how to prepare a bank reconciliation statement.

One is making a note in your cash book (faster to do, but less detailed), and the other is to prepare a bank reconciliation statement (takes longer, but more detailed). When you record the reconciliation, https://www.accountingcoaching.online/ you only record the change to the balance in your books. The change to the balance in your bank account will happen “naturally”—once the bank processes the outstanding transactions.

All of your bank and credit card transactions automatically sync to QuickBooks to help you seamlessly track your income & expenses. However, you typically only have a limited period, such as 30 days from the statement date, to catch and request correction of errors. Get a close-up view of how accounting on Salesforce can eliminate the need for costly integrations—and silos of mismatched information—by sharing the same database as your CRM.

It’s near impossible to have confidence in your bank account balances when the person preparing the reconciliation and validating the amounts is bogged down by spreadsheets. In short, how often a company should prepare bank reconciliations depends on the level of activity in its bank accounts. For companies with a high number of bank transactions, preparing it every month or, if possible, several times in a month is better.

The first step involves identifying any deposits and checks that the bank has not processed at the statement date. Keeping your financial records in order is hugely important to the success of your business. Read the steps you should take when closing out your small business’ books for the end of the fiscal year. The Transaction Matching software utilizes AI to discover and configure matching rules, enabling automatic line-level transaction matching between different data sources. Auto-reconciling transactions reduces human errors, such as keying inaccuracies and adds security to the reconciliation process. The first step is to obtain a detailed statement from the bank, which includes information about checks cleared and rejected by the bank, transaction charges, and bank fees.

Before attempting the reconciliation write up the cash book as fully as possible by using the following process. The items therein should be compared to the new bank statement to check if these have since been cleared. They https://www.kelleysbookkeeping.com/gross-profit-operating-profi-vs-net-income/ also explain any delay in the collection of cheques, and they identify valid transactions recorded by one party but not the other. We know that taking hours to find amounts that are off by a few pennies doesn’t make sense.

While preparing bank reconciliations regularly is better than preparing it after a couple of months, if the number of bank transactions is low, companies may choose to perform it later. As mentioned above, timing differences do not require any adjustments in the bank book balance. Therefore, these items need to be part of the bank reconciliation statement only. For timing differences, the company must cancel out the effect of outstanding checks and deposits in transit. Bank reconciliation is a part of the internal control process of a company. As mentioned above, two different documents show the bank balance of a company at the end of a specific period.

A bank reconciliation statement is a summary that shows the process of reconciling an organization’s bank account records with the bank statement. It lists the items that make up the differences between the bank statement balance and the accounting system balance, and explains how these differences were resolved. Bank reconciliation is the process of comparing the balance as per the cash book with the balance as per the passbook (bank statement). The very purpose of reconciling the bank statement with your business’ books of accounts is to identify any differences between the balance of the two accounts. How you choose to perform a bank reconciliation depends on how you track your money. Some people rely on accounting software or mobile apps to track financial transactions and reconcile banking activity.

By using software tools to automate bank reconciliation, businesses can focus on other critical tasks and make informed business decisions based on accurate financial data. By avoiding these common errors, you can ensure the accuracy of your organization’s financial records, make informed business decisions, and reduce the risk of financial issues. Regular reconciliation and review of financial records can help identify and resolve errors promptly, reducing the risk of financial issues. Bank reconciliation is a subset of the monthly, quarterly, and yearly close process and is not generally done on its own. Accountants spend a lot of time on this step to ensure the checks are thorough and even minute errors are spotted.